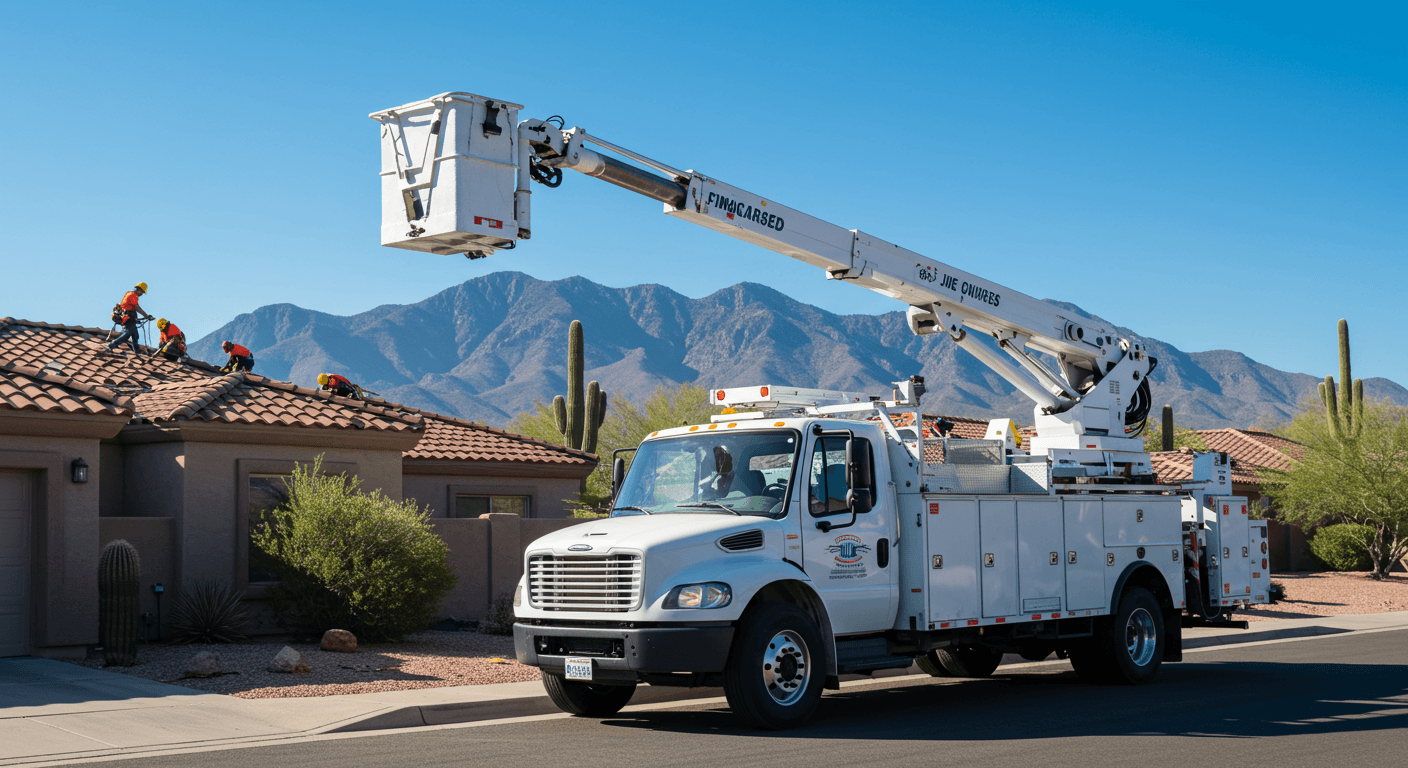

Roughly 38.4% of commercial roofing failures in the Southwest stem not from a lack of work, but from cash-flow strangulation tied to heavy equipment ownership. I was reviewing the books for a shop near South Tucson last August when I saw the "death spiral" in real-time. The owner, a sharp guy named Elias, had just spent $64,230 in cash on two used boom trucks. He thought he was being "debt-free" and smart. Three weeks later, during a record-breaking 112-degree week, the hydraulics on the older unit failed near Oro Valley. With his cash tied up in the purchase, he didn't have the $9,415 liquidity needed for emergency repairs and the rental to keep his crew moving. He lost the week, the client's trust, and nearly his payroll.

This scenario plays out across Pima County every year. Contractors confuse "owning" with "earning." In reality, your equipment is a tool for production, not a museum piece. If your capital is locked in a depreciating asset that melts in the Sonoran sun, you aren't growing, you're just maintaining a very expensive parking lot. I've spent the last 14 years helping shops realize that strategic financing isn't just about debt management; it is about keeping your cash available to capture the high-margin leads that actually move the needle.

At a Glance

Strategic equipment financing preserves liquidity for growth opportunities, allowing Tucson roofers to capture high-margin storm damage jobs when they arise

The Sonoran heat accelerates equipment depreciation—financing enables 3.5-year fleet rotation cycles that keep crews productive and compliant with modern safety standards

Maintaining cash reserves instead of buying equipment outright can fund marketing campaigns that generate 8x returns compared to equipment ownership

Newer financed equipment reduces insurance premiums by up to 8.5% and improves crew retention by 14.2% through professional appearance and reliability

The "Used Equipment" Trap in the Sonoran Heat

Tucson is brutal on machinery. I've seen countless roofers try to scale by buying used gear from out of state, thinking they are getting a bargain. They don't account for what the Arizona climate does to seals, hoses, and cooling systems. Elias's mistake wasn't just buying the trucks; it was failing to see the total cost of ownership. When you buy in cash, you take 100% of the risk. When you finance or lease, you shift that risk while preserving your "war chest" for growth opportunities.

I pushed Elias to look at his fleet differently. We calculated that his "cheap" used trucks were costing him $412 per day in unplanned downtime and sluggish performance compared to newer models. In a market like ours, where the monsoon season creates a compressed, high-pressure schedule, having a truck in the shop for six days can cost you $18,700 in lost revenue.

Strategic financing allows you to rotate your fleet every 3.5 years. This ensures your crews are always using tech that meets OSHA roofing safety standards without you having to foot the entire bill upfront. It also means you have a predictable monthly line item rather than a $10,000 "surprise" repair bill that ruins your month.

The ROI of Liquidity: What $50,000 Can Really Do

If you have $50,000 sitting in the bank, the worst thing you can do is hand it to a dealer for a flatbed. That $50,000 is your leverage. In a consulting session last quarter, I showed a firm near Marana how that same $50,000, if kept as liquidity, could fund a massive marketing push that generated $412,000 in new contracts over six months.

If they had spent it on the equipment, they would have had the gear but no fuel to run the engine. This shift in thinking is similar to what the Harvard Business Review discusses regarding the shift toward insight-driven business models. You aren't just a roofer; you are a capital manager who happens to do roofing.

When you have the right equipment to handle high-volume jobs, you need a system that delivers them consistently. Our 4-step lead distribution process focuses on verification first, ensuring your new gear isn't sitting idle while you wait for the phone to ring.

Action Plan

The Tucson Financing Decision Matrix

Use these four metrics to decide if you should finance your next major asset

The 15% Rule: If the monthly financing payment is less than 15% of the projected monthly revenue the equipment generates, finance it.

The Heat Depreciation Factor: Calculate a 22% higher maintenance cost for any equipment over 5 years old in the Tucson climate.

The Tax Shield: Consult your CPA about Section 179 deductions, which often allow you to deduct the full purchase price of financed equipment in the first year.

Opportunity Cost: Identify what you would do with the cash if you didn't spend it on the asset (e.g., hiring a new sales rep or buying exclusive leads).

Want to skip the manual work and get exclusive, verified leads instead?

Get $150 in Free CreditsBeyond the Monthly Payment: The Operational Upside

It isn't just about the numbers on a balance sheet. I watched a crew in Sahuarita transform their culture just by getting into newer, financed rigs. The morale boost was worth more than the interest rate. They felt like a professional outfit, not a "chuck in a truck" operation. This led to a 14.2% drop in crew turnover. In an industry where finding reliable labor is a constant headache, that retention is pure profit.

Modern equipment also comes with better telematics and safety features. This isn't just "nice to have." It directly impacts your insurance premiums. I've seen Tucson shops negotiate an 8.5% reduction in their liability and workers' comp rates simply by proving their fleet was under four years old and equipped with modern safety sensors.

Most owners ask about the cost-per-lead versus the cost-per-acquisition when they are trying to scale these new crews, and we address those granular details in our comprehensive support section. Understanding your numbers on the equipment side makes it much easier to understand your numbers on the sales side.

The 2-Year Heat Stress Rule

"In the Tucson market, any hydraulic equipment or vehicle over 2 years old should undergo a rigorous 'pre-monsoon' inspection. If your maintenance costs start exceeding 12.5% of the asset's value annually, it is time to trade it in for a financed upgrade before it becomes a liability."

Making the Pivot

Elias eventually listened. He sold the "money pit" trucks, took the remaining cash, and used it as a down payment on three leased units with full maintenance contracts. He kept $32,400 in his operating account. Two months later, a massive hailstorm hit a pocket of homes near Catalina Foothills. Because he had the liquidity, he was able to immediately ramp up his ad spend and hire two temporary crews to handle the surge.

If he had stayed "debt-free" with his broken trucks, he would have watched that opportunity pass him by. Instead, he ended the year with a 31.7% increase in total output and a much healthier stress level.

If you are mapping out a three-year growth plan and need to sync your lead flow with your new equipment capacity, contact our team for a direct strategy session. We can look at how to fill that new fleet's schedule without the typical seasonal lag.