Years of looking at P&L statements taught me that a $3.7 million top line in the Bull City doesn't mean a thing if your bank account is sitting at four figures on payday. Sitting across from Gavin at a small table near the American Tobacco Campus, I watched him stare at a spreadsheet that showed $412,843 in accounts receivable while he worried about covering his $14,200 weekly payroll. He wasn't failing; he was growing, but he was growing his way into a shallow grave because his cash velocity couldn't keep up with his crew's speed.

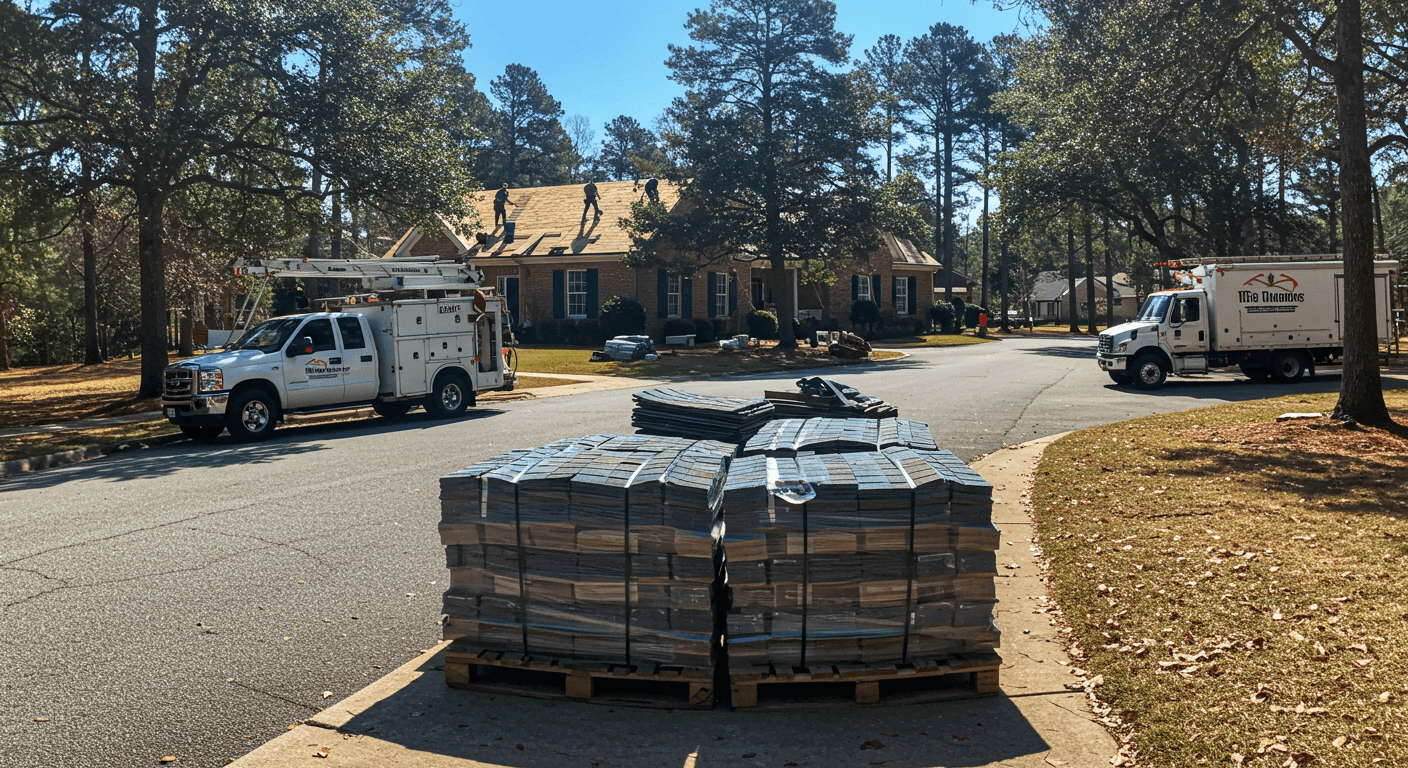

What Gavin experienced in the Durham market is a trend I'm seeing across the Research Triangle. We're in a high-demand pocket where new construction in areas like Brier Creek and residential flips in Old North Durham are exploding. But high demand often masks a dangerous reality: the "growth gap." This is the time between when you pay for a stack of GAF shingles and a crew's labor on a job near Duke Forest, and when the final check actually clears your Atlantic Union Bank account. For Gavin, that gap was stretching to 34 days, creating a liquidity vacuum that nearly choked his operation.

North Carolina roofing companies face significant margin pressure from cash flow gaps, making optimized billing strategies critical for profitability.

At a Glance

Implement a 40/40/20 milestone billing structure to front-load material and mobilization costs.

Shift from 'spray and pray' marketing to high-intent leads to shorten the sales-to-cash cycle.

Use automated AR follow-ups to reduce average collection times from 31 days to under 17 days.

Factor Durham-specific permitting delays (currently 12.3% longer than 2022) into cash forecasts.

The Durham "Growth Trap" and Market Volatility

Durham is currently experiencing a construction surge that is both a blessing and a curse. According to recent reporting from Construction Dive, labor costs and material delivery schedules are fluctuating wildly across the Southeast. For a roofer working a residential patch in Hope Valley, this means that a quote given 45 days ago might now be $2,100 under-priced due to a sudden spike in plywood or fuel surcharges.

The trend I'm analyzing with my clients isn't just about inflation; it's about the cost of capital. When your cash is tied up in "work in progress" (WIP), you're essentially giving your customers an interest-free loan. In a market where interest rates for operational lines of credit have climbed, that "loan" is costing you about 9.4% more than it did three years ago.

I advised Gavin to stop looking at his business as a roofing company and start looking at it as a financial engine. If the engine doesn't have oil (cash), the gears (crews) seize up. We looked at his overhead and realized he was spending $3,842 a month on lead sources that took 60 days to convert. That's a massive drag on cash flow.

Rethinking the Billing Lifecycle

Most contractors in North Carolina still operate on the "deposit and final" model. You take 10% or 20% down, then wait for the final inspection to get the rest. In Durham, where the City-County Planning Department is often backed up, waiting for that final sign-off to trigger a $12,000 payment can be a death sentence for your margins.

Instead, we transitioned Gavin to a milestone-based system.

- Material Drop (40%): This covers the shingles, underlayment, and delivery fees. You aren't out of pocket for the physical goods.

- Tear-Off/Dry-In (40%): Once the old roof is off and the house is protected, you collect the bulk of your labor costs.

- Completion/Inspection (20%): The final "cherry on top" that represents your true profit.

By moving the bulk of the cash collection to the start of the job, Gavin's bank account stayed "green" throughout the project.

Traditional vs. Milestone Billing

| Factor | Traditional Billing (Deposit/Final) | Milestone Billing (40/40/20) |

|---|---|---|

| Cash Out-of-Pocket | High (Labor/Materials) | Low (Materials covered early) |

| Risk of Non-Payment | 80-90% of job total | 20% of job total |

| Payroll Pressure | Intense on Fridays | Manageable and predictable |

| Durham Permit Delay Impact | High (Final check held up) | Low (80% of funds already in) |

Cash Out-of-Pocket

Risk of Non-Payment

Payroll Pressure

Durham Permit Delay Impact

Lead Quality and its Impact on Cash Velocity

One of the most overlooked aspects of cash flow management is the quality of your pipeline. If your sales team is spending 14 hours a week chasing "maybe" leads from a generic list, your acquisition cost per job (CAC) skyrockets. More importantly, those "tire-kicker" leads have a longer sales cycle.

I've seen contractors transform their pipeline by moving toward verified, exclusive opportunities. When you aren't fighting five other guys for the same roof in Southpoint, your close rate goes up and your "time-to-contract" goes down. This is why understanding how lead distribution works is critical for owners who want to stabilize their revenue. The faster you move from lead to contract, the faster the cash hits your ledger.

The 72-Hour AR Rule

"Never let a completed job sit for more than 72 hours without a digital invoice and an automated follow-up. In Durham's fast-paced market, homeowners get distracted. A friendly, automated text reminder on day three can reduce your 'Days Sales Outstanding' by 18.2%."

Labor Trends and the Retention Cost

Labor is the biggest variable in the roofing cash flow equation. The Western States Roofing Contractors Association has highlighted that while safety and training are paramount, the administrative burden of managing sub-crews is a hidden profit eater.

In Durham, competition for skilled labor is fierce. If you're late on a payroll by even 24 hours because a client's check didn't clear, you risk losing your best crew to a competitor working the NC-55 corridor. Gavin nearly lost his top foreman, Xavier, because of a three-day delay in a progress payment. We fixed this by setting up a "Labor Reserve" fund—a separate high-yield savings account that holds exactly 2.5 weeks of payroll at all times. This acts as a shock absorber for the business.

Action Plan

A 4-Step Framework to Insulate Your Roofing Business from Cash Flow Gaps

A systematic approach to protecting your Durham roofing operation from cash flow gaps during high-growth periods.

The 'Daily Cash Flash': Spend 4 minutes every morning checking three numbers: Bank Balance, Pending Deposits, and Payroll Liability for the next 14 days. Don't rely on your bookkeeper for this; own the data.

Vendor Terms Negotiation: Ask your material suppliers for Net-30 or even Net-45 terms. If you can get paid by the homeowner in 15 days but don't have to pay for the shingles for 30 days, you've effectively created 'negative working capital,' which is the holy grail of cash flow.

High-Efficiency Lead Sourcing: Cut the waste. If a lead source isn't producing a signed contract within 11 days, it's a drain on your cash. Focus on verified leads that allow for locked previews so you aren't buying garbage.

Digital Payment Adoption: Stop accepting paper checks for anything over $5,000. Use a portal that allows for ACH or credit card payments (with a convenience fee passed to the homeowner). This shaves 4.2 days off your collection time compared to waiting for 'the check in the mail.'

Want to skip the manual work and get exclusive, verified leads instead?

Get $150 in Free CreditsThe Hidden Danger of Seasonality in NC

While North Carolina doesn't have the brutal winters of the North, we do have the Atlantic hurricane season and the "Spring Squeeze." From March to May, every homeowner in Durham realizes their roof leaked during the winter rains. This creates a massive spike in work, which requires a massive spike in cash for materials.

Many owners make the mistake of over-leveraging during these peaks. I've seen shops take out high-interest EIDL loans or merchant cash advances to cover material costs for a big storm run. The math rarely works out. A 14.7% interest rate on a short-term loan can wipe out your entire net profit on those jobs.

If you're unsure about how to price for these seasonal shifts, checking a comprehensive FAQ on lead costs and quality can help you budget your marketing spend so you aren't over-extending when your crews are already at 105% capacity.

Avoid 'Robbing Peter to Pay Paul'

Never use the deposit from Job B to pay for the materials on Job A. This is the most common reason roofing companies in Durham fail. Once the music stops and new jobs slow down, the whole house of cards collapses.

Looking Forward: 2025 Projections

The trend for the next 18.5 months suggests that Durham will remain a "seller's market" for roofing services, but only for those who can manage their backend. We're seeing a shift toward "Roofing as a Service" models where maintenance contracts provide a steady, predictable monthly income to offset the lumpy nature of replacement jobs.

I told Gavin that his goal shouldn't be to hit $5 million next year. His goal should be to hit $4.2 million with a 12% higher cash reserve. When he stopped chasing every lead and started focusing on the jobs that paid within his milestone window, his stress levels plummeted. He even started taking weekends off again to spend time at Sarah P. Duke Gardens—something he hadn't done in 3.5 years.

If your current lead flow is creating more headaches than profit, or if you're tired of fighting the cash flow battle alone, it might be time to look at a more verified approach to growth. Whether you need to tighten up your billing or you're ready to contact a growth specialist to talk about scaling your Durham operations, the first step is admitting that revenue is vanity and cash is reality.