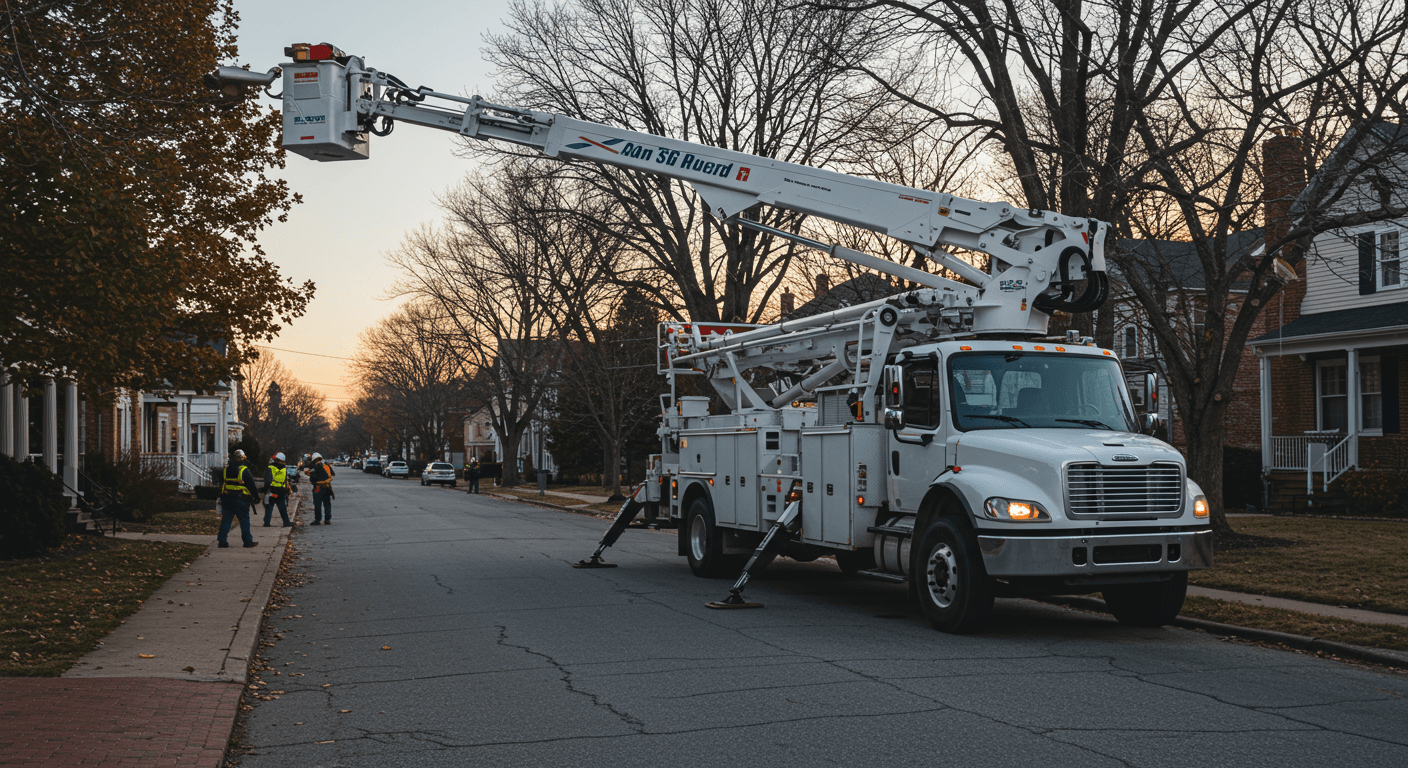

Walking past a row of idling trucks near the Goodyear Heights neighborhood, I watched Xavier pull a crumpled invoice from his glove box. The paper detailed a $13,642 repair bill for a crane truck that had spent more time in the shop than on job sites this quarter. Xavier looked at the aging fleet, then at the I-76 traffic, and asked the question that keeps most Akron shop owners up at night: "Do I keep patching these up, or do I take on $240,000 in debt for new rigs?"

This moment happens in every growing roofing business. It is the pivot point where you stop being a contractor and start being a fleet manager and financial strategist. In the Akron metro area, where the season is compressed by unpredictable lake-effect weather, equipment uptime is not just a convenience. It is the difference between hitting your year-end revenue targets and losing 18.4% of your potential margin to delays and maintenance.

At a Glance

Financing equipment allows you to preserve working capital for rapid-response marketing and emergency payroll during slow weather months.

Leasing often provides a better tax shield for high-growth companies, while purchasing builds long-term equity for business valuation.

Modern equipment reduces labor costs by an average of 14.7% through faster site setup and reduced manual material handling.

Local market conditions in Akron require high-reliability fleets to maximize the 8.5-month peak production window.

The Akron Market Context: Why Equipment Strategy Matters Now

Our local market in Northeast Ohio is currently witnessing a unique shift. While some residential sectors have cooled, the demand for high-efficiency roofing systems in suburbs like Fairlawn and Bath remains aggressive. According to recent data from IBISWorld's roofing industry analysis, the roofing industry continues to face volatility in material costs, making operational efficiency the primary lever for profit protection.

When I analyzed Xavier's books, we found that his older equipment was costing him $2,180 per month in "invisible" losses. This included extra labor hours when a lift failed and the crew had to hand-carry shingles, plus the opportunity cost of missed jobs because he could not commit to a tight timeline. In a city where the "Rubber City" legacy means we respect hard work and durability, having a fleet that looks and acts professional is also a branding tool. If your trucks are leaking oil on a $35,000 driveway in West Akron, you are losing more than just a repair fee.

Calculating the True ROI of New Equipment

The mistake I see most often is looking only at the monthly payment. To make a real business decision, you have to look at the total cost of ownership (TCO) compared to the revenue-generating potential of the asset.

Let's look at a real-world scenario we modeled for a shop operating near Firestone Park. They were considering a new $87,450 specialized shingle buggy and trailer setup.

- Labor Savings: The new setup allowed a 5-man crew to finish 1.5 hours earlier each day. At a fully burdened labor rate of $38 per hour, that is $285 per day in savings.

- Production Speed: Over a 22-day working month, those hours added up to 33 saved hours, enough to squeeze in two extra small repair jobs or one additional mid-sized reroof.

- Total Monthly Gain: Between labor savings and the added revenue from the extra jobs, the equipment "earned" the company $5,340 per month.

- The Payment: A 60-month lease at 7.2% interest put the payment at approximately $1,738.

The math was clear. The equipment was not an expense. It was a net gain of $3,602 per month after the debt was serviced. When you see numbers like that, the fear of the "big loan" starts to evaporate. It is about shifting your perspective from "what does this cost" to "what does this enable."

If you are currently trying to decide if your lead flow justifies this kind of expansion, it helps to see how others are handling their pipeline. Many of the successful owners I consult with use exclusive, verified leads to ensure that when they do invest in a new $120,000 boom truck, it stays busy five days a week.

Faster site setup and reduced manual material handling translate directly to improved profit margins.

Lease vs. Buy: The Great Contractor Debate

There is no one-size-fits-all answer, but there are clear winners depending on your tax situation. In my experience working with Northeast Ohio firms, the decision often comes down to your five-year exit plan.

Purchasing equipment using a traditional commercial loan is the gold standard for owners who want to build a "heavy" balance sheet. If you plan to sell your company in seven years, having a fleet of ten fully-owned, well-maintained trucks adds significant "blue sky" value to the business. You also get the benefit of Section 179 depreciation, which can be a massive win if you have had a high-profit year and need to lower your tax liability.

Leasing, on the other hand, is for the "lean" operator. Construction Dive has noted that many firms are moving toward leasing to stay ahead of the technology curve. In the roofing world, this means having the newest safety features and the most fuel-efficient engines. For Xavier, we looked at a fair market value (FMV) lease. This kept his payments lower than a purchase and allowed him to trade in the trucks every 3.5 years. In the salt-heavy winters of Akron, trading in a truck before the frame starts to rust out is a strategic move that many owners overlook.

Equipment Leasing vs. Traditional Financing

| Factor | Traditional Financing (Buying) | Equipment Leasing |

|---|---|---|

| Upfront Cost | Often 10-20% down | Usually 0-5% down |

| Monthly Payment | Higher, includes interest and principal | Lower, tax-deductible as expense |

| Maintenance | Owner's responsibility | Often bundled in the lease |

| Tax Benefit | Depreciation over 5-7 years | Immediate deduction of payments |

| End of Term | You own the asset outright | Return or buy at market value |

Upfront Cost

Monthly Payment

Maintenance

Tax Benefit

End of Term

Managing the Debt-to-Income Ratio

One thing that keeps local bankers in Akron nervous is a contractor who over-leverages during a boom year. I always advise my clients to keep their total debt service under 12.4% of their gross monthly revenue.

When Xavier wanted to buy three trucks at once, we looked at his seasonal dips. Akron winters are brutal for cash flow. If your debt payments are $12,000 a month but your revenue drops to $45,000 in January, you are in the "danger zone." We opted for a "step-up" payment plan where his payments were lower in the winter and slightly higher in the summer. Not every lender offers this, but for seasonal businesses like roofing, it is a lifesaver.

Managing this balance requires a steady stream of work. I've seen shops get into trouble when they buy the gear but forget to fuel the sales engine. If you find your calendar has too many white spaces, you might want to browse our growth resources to see how to stabilize that incoming job volume before signing a new five-year note.

The 72-Hour Maintenance Rule

"Before financing any piece of equipment, call three local repair shops in the Akron area. Ask them their current lead time for hydraulic or engine repairs on that specific model. If they cannot guarantee a 72-hour turnaround for commercial clients, that equipment is a liability, not an asset. A $2,000 monthly payment is manageable; a $2,000 payment on a truck that has been sitting in a lot on Romig Road for three weeks is a business killer."

Interest Rates and Timing the Market

We are currently in a "higher for longer" interest rate environment. This has made some contractors hesitant to pull the trigger. However, waiting for a 1% drop in rates might cost you more in lost efficiency than you save in interest.

If you are financing $100,000, a 1% difference in interest is roughly $1,000 a year. If that new equipment saves you just two hours of labor a week, you have already recouped that difference. Don't let a "macro" headline stop you from making a "micro" improvement to your profit margin.

I also recommend looking at local credit unions in Summit County. Often, they have a better understanding of the local construction landscape than the big national banks. They know the names of the neighborhoods you are working in, and they understand that a roofing company in Akron is a solid bet because of the constant need for storm repair and maintenance in our climate.

Final Thoughts on Scaling Your Operations

Scaling a roofing business is like climbing a ladder; you need one hand on your operations and one hand on your finances. If you move one too far without the other, you lose your balance.

Xavier ended up financing two new trucks and selling his older crane for parts. The result? His fuel costs dropped by 9.6% and his "emergency repair" budget went to zero. Most importantly, his crew felt like they were working for a winning team. That psychological boost is hard to quantify on a spreadsheet, but it shows up in the quality of the shingles being laid in neighborhoods from Tallmadge to Stow.

If you are feeling overwhelmed by the technicalities of growth, you are not alone. Sometimes the best move is to talk to someone who sees the backend of hundreds of shops. You can always reach out to our team to discuss how to align your lead volume with your new equipment capacity.